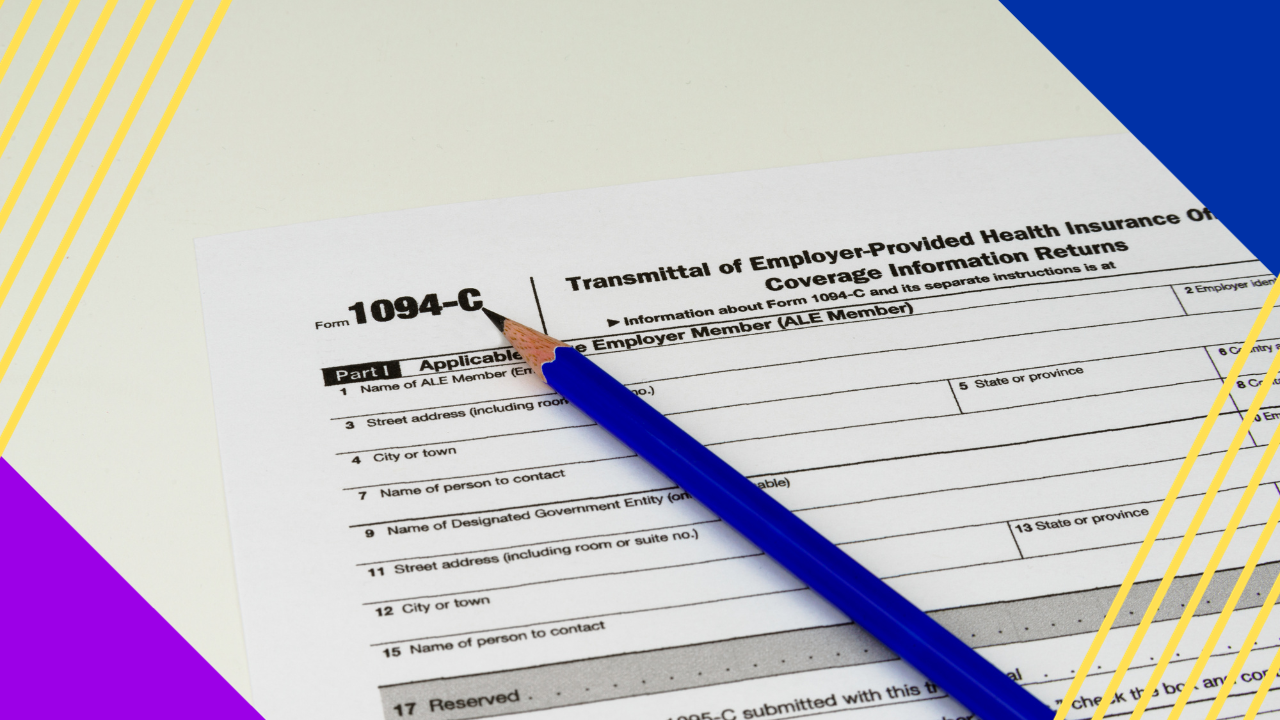

An overview of Form 1094-C

Form 1094-C is a crucial document in the realm of tax compliance.

Employers need to understand and accurately complete it when it comes to reporting their health insurance offers and coverage to the Internal Revenue Service (IRS).

This intricate and often misunderstood form is essential for businesses in properly documenting their compliance with the Affordable Care Act’s (ACA) employer mandate.

In this article, we’ll look at the specifics of Form 1094-C, deciphering its purpose, components, and the key information that employers need to know when filing.

What is Form 1094-C?

Form 1094-C, also known as the Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns, is used by employers to report information about the following:

- Offers of health coverage made to their employees

- The number of employees enrolled in the coverage

- Other information related to employee health care coverage

Form 1094-C is submitted to the IRS to fulfill reporting obligations under the Affordable Care Act of 2010. It’s accompanied by employee statements on Form 1095-C.

The information on Form 1094-C helps the IRS monitor and enforce the employer-shared responsibility provisions outlined in the ACA.

Form 1094-C vs. Form 1095-C

Form 1094-C and Form 1095-C are both required by the IRS to monitor employer compliance with the ACA. While both are related to reporting health coverage information, they serve different purposes.

Form 1094-C acts as a cover sheet for the more detailed Form 1095-C. This form is sent only to the IRS and provides a summary of the information contained in the latter form.

It’s essentially an overview for the IRS to assess whether the employer has met ACA requirements.

Form 1095-C is also known as the Employee-Provided Health Insurance Offer and Coverage Statement. Employers use this form to provide detailed information to each of their full-time employees about the health insurance coverage offered during the tax year.

Form 1095-C is distributed among employees and sent to the IRS.

Form 1094-C is a higher-level summary that is filed to the IRS, whereas Form 1095-C primarily focuses on information related to specific employees.

Who must file Form 1094-C?

If you fall under the category of applicable large employer (ALE), then you are required to submit Form 1094-C. An ALE generally has 50 or more full-time employees during the year, including equivalent employees.

ALEs must complete and file 1094-C annually to ensure accurate reporting and avoid potential penalties associated with non-compliance. Outsourcing tax accounting can be beneficial in this venture.

How to fill out Form 1094-C

Here is a brief guide on how to fill out Form 1094-C:

- Part I – Enter all information regarding the ALE member, including the name, address, and Employer Identification Number (EIN).

- Part II – Enter the information that will qualify the ALE member to file the form. This part only gets completed in the authoritative form.

- Part III – This part concerns information on your Certificates of Eligibility, which employees are impacted, and which coverage codes you’ll use on Form 1095-C.

- Part IV – If you’re a member of an aggregated ALE group, fill in the information in this part.

It’s important to carefully review the instructions for Form 1094-C provided by the IRS to ensure accurate completion and filing.

Note that the instructions and requirements may change each tax year, so refer to the most up-to-date information.

When to submit Form 1094-C

Form 1094-C is submitted to the IRS annually. The specific deadline is generally the same as the deadline for filing individual employee statements on Form 1095-C.

Take note of the following deadlines:

- If filing on paper – The deadline for Form 1094-C is typically February 28th of the year following the tax year being reported.

- If filing electronically – The deadline for Form 1094-C is typically March 31st of the year following the tax year.

Employers are encouraged to file electronically if they are submitting at least 250 forms.

These deadlines may be subject to change or extensions under certain circumstances. Employers may request an automatic 30-day extension by submitting Form 8809 on or before the due date of the returns.

Penalties for misfiling Form 1094-C

Misfiling Form 1094-C can result in penalties imposed by the IRS. The exact penalties vary based on the nature and severity of the errors.

Potential penalties include:

Failure to file. If an ALE fails to file Form 1094-C by the deadline, it may incur a penalty. This sanction is assessed per return, and the amount depends on how late the filing occurs and the size of the employer.

Failure to furnish. If an ALE fails to furnish the Form 1095-C statements along with Form 1094-C, this will result in a separate penalty per statement not furnished.

Intentional disregard. If the IRS determines that an employer intentionally disregards the filing or furnishing requirements, it may impose a higher penalty.

Inaccurate or incomplete information. Penalties may be assessed if the information provided on the submitted Form 1094-C is inaccurate or incomplete. If the ALE does not correct the error in a timely manner after being notified by the IRS, it will be subject to penalties.

Penalty amounts are subject to change, and it’s crucial to refer to the most recent IRS guidance for the specific amounts and rules.

To mitigate the risk of penalties, employers may consider seeking guidance from tax professionals or using specialized tax software to facilitate compliance.

Independent

Independent